We have No Action Items again today

Summary of Issues

At Issue 1. we see COLA INCHES TOWARDS ZERO. Modest growth can’t get COLA out of red. Weak energy and a strong dollar keep the January Consumer Price Index low. (See Issue 1 below for the details. GF)

At Issue 2. we see NEW TRICARE FEES COULD BE COMING TO YOU Budget hikes copays, enrollment fees, deductibles, TRICARE beneficiaries continue to be targets in budget-balancing schemes. (See Issue 2 below for the details. GF)

At Issue 3. we see WITH PROPOSED TRICARE CHANGES, TIME IS NOT ON YOUR SIDE. It’s not just the fees, it’s how they’re adjusted. In his February As I See It column, MOAA Director of Government Relations Col. Steve Strobridge, USAF (Ret), highlights how a less-apparent aspect of DoD-proposed health care fee changes could really bite you. (See Issue 3 below for the details. GF)

At Issue 4. we see MOAA’S ANNUAL LETTER. This year promises to be a big one for military health care

Find out how MOAA is striving to secure the future of our servicemembers and their families in 2016. (Click on MOAA’S ANNUAL LETTER here or above for the details. GF)

Collectively We Can and Are Making a Difference

FOR ALL, Please feel free to pass these Weekly Legislative Updates on to your group of Veteran Friends –

don’t be concerned with possible duplications – if your friends are as concerned as we are with Veteran issues, they probably won’t mind getting this from two or more friendly sources

ISSUES

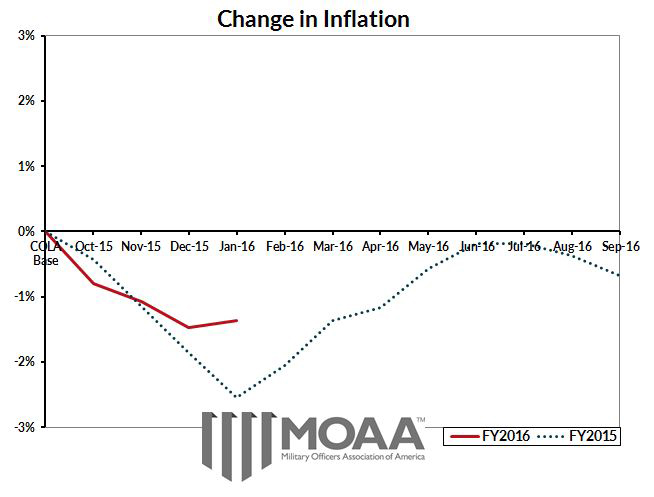

Issue 1. COLA INCHES TOWARDS ZERO

In order for a positive COLA next year, the Consumer Price Index (CPI) has to make pretty significant increases.

COLA remains in the red, but is up slightly from last month.

The January CPI is 231.061, increasing marginally to 1.4 percent below the FY 2014 COLA baseline. Because there was not a positive COLA in FY 2015, the FY 2014 baseline is used.

The CPI for February 2016 is scheduled to be released on March 16, 2016.

Note: Military retiree COLA is calculated based on the CPI for Urban Wage Earners and Clerical Workers (CPI-W), not the overall CPI. Monthly changes in the index may differ from national figures reported elsewhere.

Related content: Retired Pay vs Active Duty Pay Adjustments

(Click on Retired Pay vs Active Duty Pay Adjustments here or above to see the details GF)

Issue 2. TRICARE REFORM, OR JUST FEE INCREASES?

February 19, 2016

Last week’s legislative update opined the proposed FY17 DoD budget was light on specifics to improve value for beneficiaries – but heavy on across the board TRICARE fee increases.

(Click on but heavy on across the board TRICARE fee increases here or above after scanning below to see more detail GF)

We also promised you more details on how these complicated budget proposals would affect various categories of beneficiaries.

We’ll start with TFL, which covers uniformed services beneficiaries age 65 and above, and certain other severely disabled retirees who are eligible for Medicare.

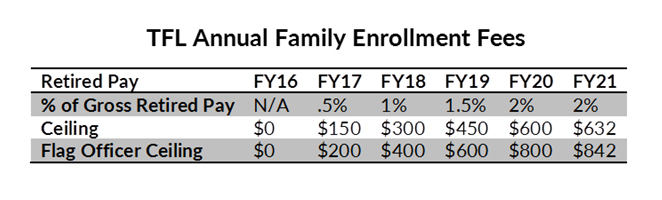

The budget proposes future TFL-eligibles – specifically, those who become Medicare-eligible on or after Jan. 1, 2017 – would have to start paying an annual enrollment fee based on a percentage of the sponsor’s retired pay.

Under this proposal, beneficiaries already enrolled in Medicare on Jan. 1, 2017 would be exempted from the new fee. (You can draw your own conclusions whether that exemption might be reconsidered in the future.) Chapter 61 retirees and survivors of servicemembers who died on active duty also would be exempt from the new fee.

The annual enrollment fee would start at 0.5 percent of gross retired pay in 2017, increasing to 2 percent of retired pay by 2021. In the first year, the fee would be capped at $150 for lower grades and $200 for retired flag and general officers. As the fee increased to 2 percent of retired pay over the next four years, those caps also would increase, reaching $632 and $842 annually in 2021.

The chart below shows the schedule of increases for the first five years. The fees shown would be for a married couple, both eligible for Medicare. Singles would pay half the rate indicated.

MOAA is particularly concerned at this plan to means-test service-earned health care benefits. No other employer means-tests retired employees’ health benefits.

MOAA objects to such means-testing, which would impose successively greater financial penalties for longer and more successful service.

It is particularly inappropriate to seek to impose additional fees on TFL-eligibles for three other reasons.

First, this population is already paying the highest fees of any military beneficiaries, as TFL requires enrolling in Medicare Part B and paying the associated premiums, which start at $2,500 per year for a married couple and can run far higher.

Second, the expressed intent of Congress in enacting TFL was that Medicare Part B premiums would be the only enrollment fee for TFL, acknowledging that Medicare would be paying 75 percent of these beneficiaries’ health costs. DoD and Hill leaders at the time opined that a career of service and sacrifice constituted a full, pre-paid premium for TFL coverage of the other 25 percent.

Third, the Pentagon’s costs for TFL have dropped dramatically – from $11 billion in FY11 to an estimated $6.4 billion in FY17, as Defense actuaries now have 15 years of actual experience with the program and can more accurately project program costs. Rather than “spiraling out of control,” DoD health costs for this group are spiraling downward – so why the need to charge them an additional fee?

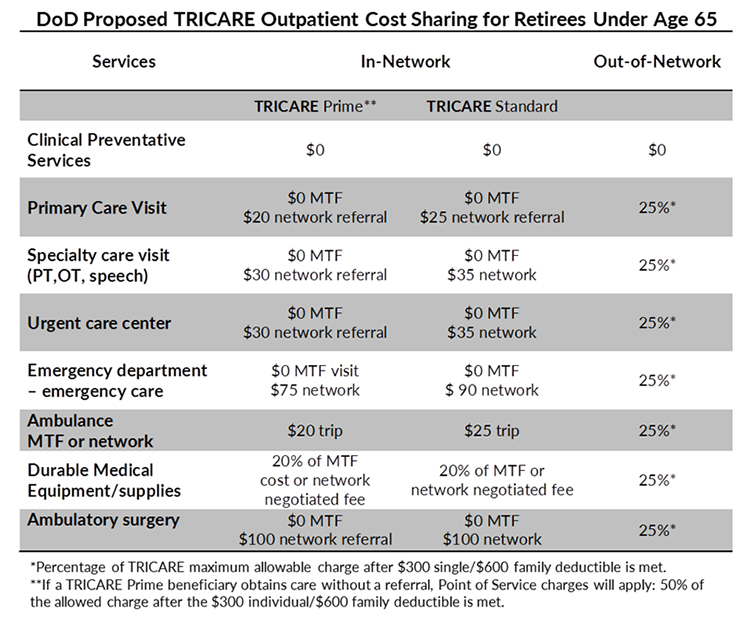

Retirees under age 65 will also see huge increases under the budget plan, with lots of fee and copay changes. Among the more complex changes are proposed cost-shares for various kinds of provider visits.

TRICARE Prime enrollees would see some increases in fees for seeing civilian network providers. TRICARE Standard beneficiaries would pay flat fees (and would not have a deductible) if they see civilian providers in the network. If they see out-of-network providers, they would still pay 25 percent of TRICARE-allowed charges, but would see their current deductible doubled – from $150/$300 (single/family) to $300/$600.

The chart below summarizes the various cost-share changes for different types of provider visits.

Prime beneficiaries who use out-of-network care without a referral would be subject to steep point-of-service fees: 50 percent of allowable charges after paying a $300/$600 deductible.

In addition, the DoD plan proposes charging all military retirees under age 65 an annual enrollment fee for participating in either TRICARE Prime or Standard. The Prime enrollment fee would rise to $350/$700 (single/family) vs. the current $283/$565.

The new enrollment fee for Standard would be even higher – $450/$900 (single/family) – plus the $300/$600 deductible for out-of-network care.

Retiree copays and cost sharing also would apply to survivors (except those whose sponsors died on active duty) and TRICARE Young Adult beneficiaries with a retired sponsor.

TRICARE Select and TRICARE Retired Reserve beneficiaries would continue their current premium levels, and their deductible and cost-shares would be the same as proposed for TRICARE Standard.

Care in Military Treatment Facilities (MTF) would continue to be provided at no cost.

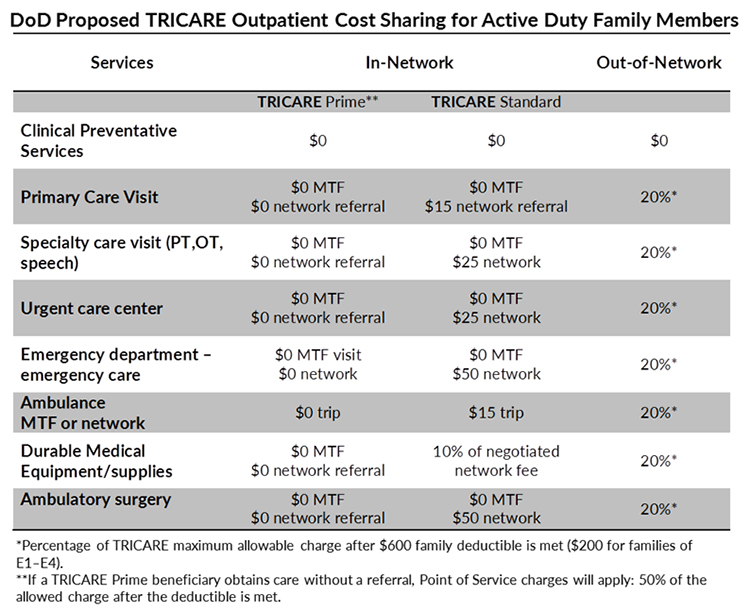

Active duty family members would not see the same drastic increases, unless they use out-of-network providers, in which case they also would incur the $600 family deductible (and high point-of-service charges if they don’t have a referral).

Active duty family copays and cost sharing would apply to survivors whose sponsors died on active duty, TRICARE Young Adult beneficiaries with an active duty sponsor, and the Transitional Assistance Management Program.

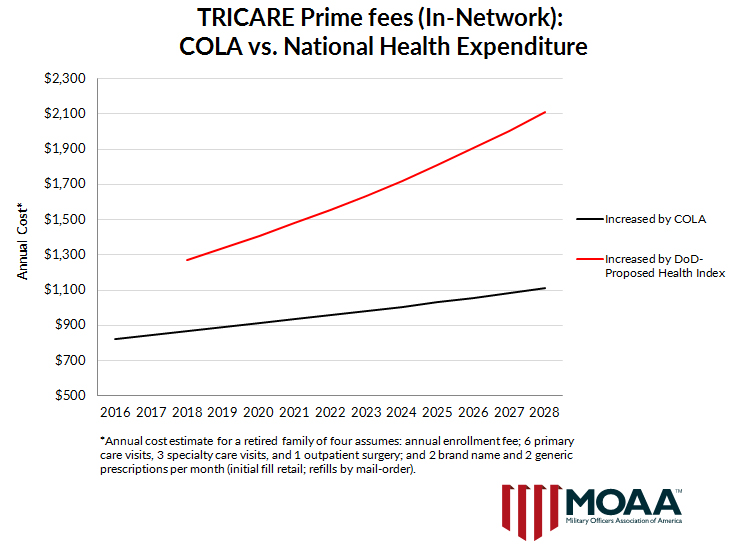

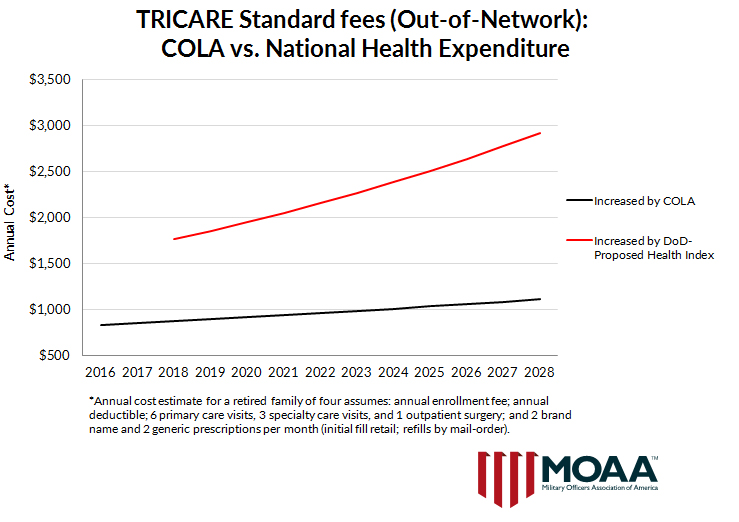

All fees, deductibles, and copays for all categories of beneficiaries would be increased annually by a national health care expenditure index, projected to rise over 5 percent annually. See this month’s As I See It column for an assessment of the impact this would have over time.

Needless to say, MOAA believes this wide array of fee increases would impose disproportionate financial penalties on retired military beneficiaries.

In addition to our concerns about the fees, we want to see more details on how DoD plans to improve beneficiaries’ timely access to quality care.

Issue 3. WITH PROPOSED TRICARE CHANGES, TIME IS NOT ON YOUR SIDE

By: Col. Steve Strobridge, USAF (Ret)Director, Government Relations

Strobridge, a native of Vermont, is a 1969 ROTC graduate from Syracuse University in Syracuse, N.Y. He was called to active duty in October 1969 and began his career as a Basic Military School training officer and commander and as a military personnel officer. He subsequently served as a compensation and legislation analyst at HQ U.S. Air Force and in the Office of the Secretary of Defense as director, Officer and Enlisted Personnel Management, with intervening assignments in Thailand and Germany.

His final assignment was as chief of the Entitlements Division at HQ U.S. Air Force, with policy responsibility for military compensation, retirement and survivor benefits, and all legislative matters affecting the military community. He is a graduate of the Armed Forces Staff College and National War College.

Strobridge retired from the Air Force in January 1994 to become MOAA’s deputy director for Government Relations. In 2001, he was appointed as director of Government Relations and elected as co-chair of The Military Coalition.

He retired from MOAA in April 2013 but was recalled as Government Relations director in September 2015.

The variety of fee changes proposed in the FY 2017 DoD budget will make your head spin:

- new enrollment fees;

- new names for TRICARE Prime and Standard;

- means-tested fees (basing fees on your retired pay amount);

- different charges for seeing in-network versus out-of-network providers;

- changing some cost shares from a percentage of the doctor bill to flat fees that vary for different kinds of providers;

- adjusting fees by a new measure of health care inflation instead of the same COLA that applies to retired pay;

- and more.

Put all those changes together, and it’s tough to figure out what they mean for real people. How, exactly, would they change what you can expect to pay for your military health care coverage?

The answer, as usual, is it depends.

It depends on whether you use TRICARE Standard, TRICARE Prime, TRICARE Reserve Select, TRICARE For Life, etcetera. It depends on whether you get your care in a military facility, from a civilian doctor in the DoD network, or from a doctor who’s not in the network. It depends on how much health care you and your family use.

MOAA has prepared some examples to show how the changes would affect annual costs for various currently serving and retired military families, assuming certain levels of health care needs. Most active duty families probably would see lower costs, while most retired families would pay significantly more. (Click on examples here or above to see the examples GF)

But these are only snapshots, estimating what your costs would be in the first year if all the various changes were enacted by Congress.

The real penalty they entail lies in how they would change your share of health care expenses over time.

Under current law, selected fees and copayments are adjusted annually by the same percentage as the retired-pay COLA.

The new proposals would adjust all fees and copayments annually by a measure of health care inflation called the National Health Expenditures (NHE) index — which is projected to grow at about 5.2 percent a year.

What would that mean to you? The charts below show how annual fees for a retired family in TRICARE Prime (in-network) and a family in TRICARE Standard (out-of-network) would jump the first year (2018) and then would grow dramatically faster in future years than they would if fees stayed indexed to the retired-pay COLA.

And how about the proposal to change in-network cost-shares from a percentage of the provider’s charges to a flat fee?

When you pay a percentage of charges under TRICARE Standard, your cost share rises over time by the same percentage as the payment to the doctor. TRICARE payments to doctors are tied to Medicare’s, and Medicare payments to doctors have risen very slowly over the past decade as Congress has tried to keep a lid on health costs. That means your cost share (20 percent of allowed charges for active duty families; 25 percent for retirees) has risen slowly as well.

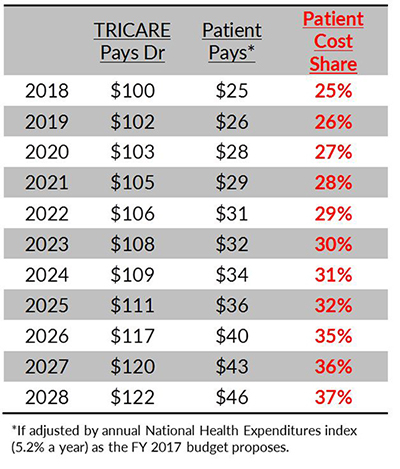

But what if your payment is switched to a flat fee that is adjusted subsequently at the rate of 5.2 percent a year, as envisioned in the defense budget proposal?

At that rate, your cost would double in about 11 years — much faster than Medicare and TRICARE payments to doctors have grown.

Let’s assume your doctor bill is $100. Your TRICARE Standard cost-share as a retiree under 65 today is 25 percent of that, or $25. That’s exactly the flat fee the new budget proposals envision for an in-network primary care visit in 2018.

But how would that change over time?

Let’s assume that $100 Medicare/TRICARE payment to the doctor grows at 1.5 percent a year — which is faster than it actually has grown in the past.

In 10 years, the TRICARE payment to the doctor would be $122, but your $25 flat fee would have grown to $46 — and instead of paying 25 percent of the doctor bill, your share would have risen to 37 percent.

No matter what you think of the initial fee changes, the biggest potential effect of these proposals, if enacted, might be how much faster they would escalate your health care costs over 20 to 30 years.

Suffice to say, time would not be on your side from that perspective.

That’s it for today- Thanks for your help!